DeFi Arbitrage in 2026: Worked Examples, Real Gas Math, and MEV-Aware Routing

Most arbitrage articles describe the idea — buy low on DEX A, sell high on DEX B — and stop there. That's not the hard part. The hard part in 2026 is that competition is dense, gas and validator tips are non-trivial, and almost every obvious arb is contested by professional searchers within the same block. This guide walks through actual numbers for a cross-DEX arb, then shows how the Vexor MEV mode quantifies extraction so you can tell a real opportunity from a 5-cent loss after costs.

A worked cross-DEX arbitrage example (Ethereum L1)

Assume USDC/WETH is briefly mispriced between Uniswap V3 (0.05% pool) and Curve TriCrypto:

- Uniswap V3 quote: 1 WETH = 3,200 USDC

- Curve quote: 1 WETH = 3,212 USDC

- Trade size: 10 WETH

Gross spread: `10 × (3,212 − 3,200) = 120 USDC`. Then subtract real costs:

- Uniswap V3 fee (0.05%): `10 × 3,200 × 0.0005 = 16 USDC`

- Curve fee (~0.04% on this pool): `10 × 3,212 × 0.0004 ≈ 12.85 USDC`

- Slippage on 10 WETH at this depth: realistically 5–15 bps each leg → assume `~20 USDC` combined

- Gas for the atomic arb contract: ~250k gas at 25 gwei × $3,200 ETH = `~$20`

- Builder/searcher tip required to land in-block ahead of competitors: typically 30–60% of expected profit. Assume `~30 USDC`

Net: `120 − 16 − 12.85 − 20 − 20 − 30 ≈ 21 USDC` per attempt. That's a real number, not the gross spread. And critically, this entire trade only works if it's atomic — submitted as a flash-loan-funded bundle so a partial fill can't strand you.

Why naive cross-DEX arb is mostly dead on Ethereum mainnet

The combination of (a) flash-loan-funded competitors, (b) builder tips eating most of the spread, and (c) sub-second mempool indexing means the only spreads that survive long enough to be capturable manually are the ones that aren't actually profitable after costs. The places real edge still exists in 2026:

- Cross-chain spreads between L1 and L2s, where bridge latency creates persistent windows.

- Long-tail tokens outside the top 200 by volume, where searcher coverage is sparser.

- Solana, where Jito bundles, lower fees, and Jupiter V6 routing change the cost structure entirely — many arbs profitable on Solana would be net negative on Ethereum L1.

- MEV strategies that capture from your own liquidity flow rather than competing for public mempool spreads.

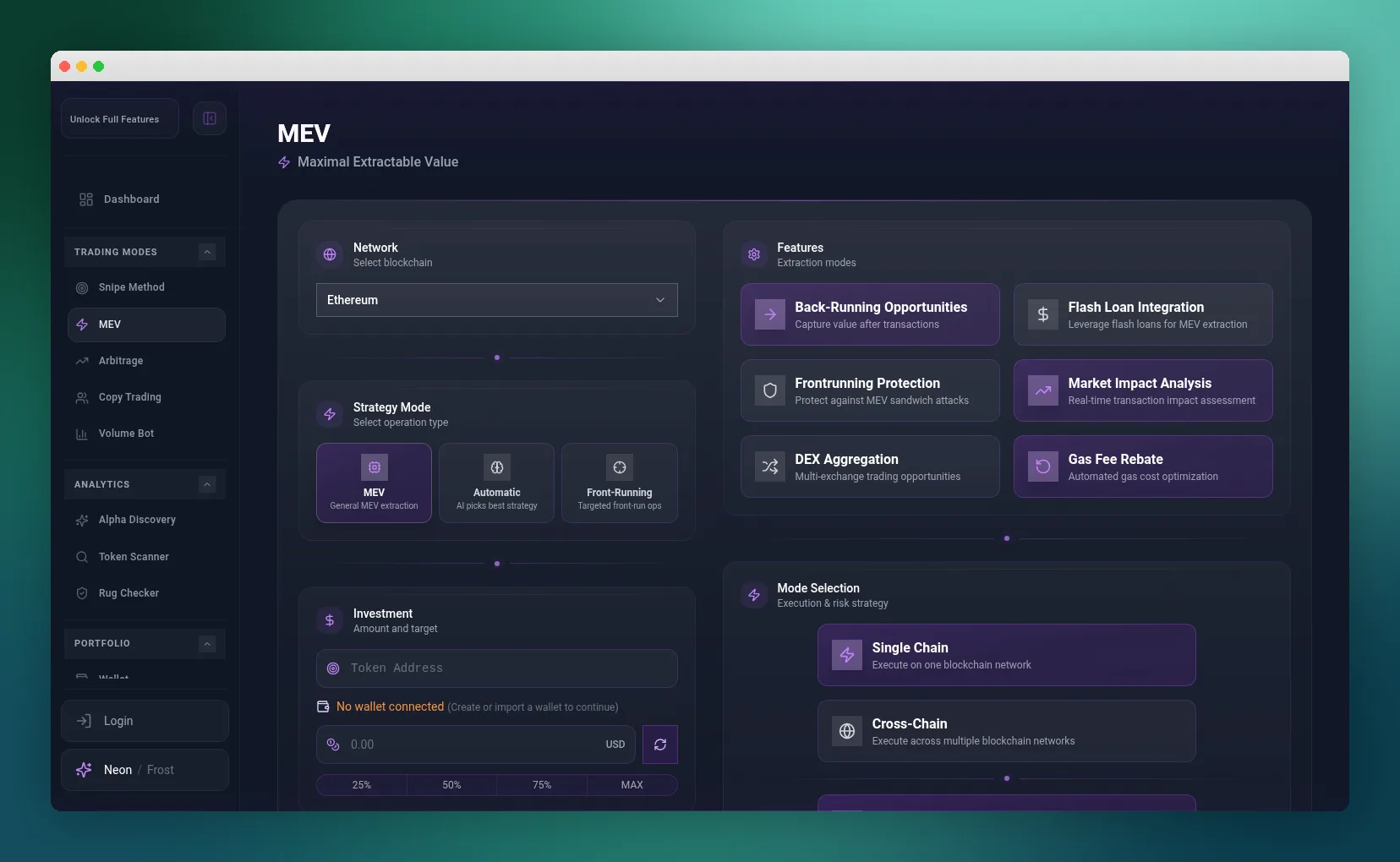

How Vexor MEV mode quantifies extraction in real time

The Vexor MEV mode is built around the idea that you should be able to see — per operation — exactly how much value is being extracted, what slippage floor is in effect, and which strategy is actually paying off. The strategy modes (Conservative, Balanced, Aggressive, Quantum) interpolate slippage tolerance, intensity, and capital deployment based on live market conditions.

What the panel surfaces that a hand-rolled arb script doesn't:

- Per-operation extraction analytics. Every MEV operation reports realized extraction, slippage actually paid, and a comparison to the Conservative baseline so you can tell whether Quantum mode is earning its higher risk budget on your specific capital base.

- Strategy-aware slippage floors. Each mode has a hard slippage floor enforced server-side. Aggressive and Quantum increase intensity multipliers but never silently raise slippage past the configured floor — this is the difference between an MEV system and a sandwich victim.

- Solana-native gas expectations. MEV runs on Solana use Jupiter V6 routes and explicit Jito tips. The minimum capital and gas expectations are documented per mode rather than hidden — you know up front whether your capital base supports the chosen mode.

- Live extraction telemetry. Real-time metrics (extraction per minute, slippage paid, success rate) replace the "set it and pray" model that most generic arb bots ship with.

Solana arbitrage with Jupiter V6 and the routing case for MEV-aware execution

The cost structure on Solana is fundamentally different from Ethereum L1, and that changes which arbs are viable. Three things matter in practice.

Jupiter V6 is the routing layer, not just a swap UI. The V6 REST API aggregates Pump.Fun bonding curves, Raydium, Orca, Meteora, and the long tail of Solana AMMs into a single best-execution route. For an arb-style trade, this matters because the spread you spotted on one DEX is rarely the spread you actually capture — V6 will route the trade across whichever combination of pools minimizes slippage, which is usually a different path than the one you eyeballed. Building Solana arbs without going through V6 means re-implementing route discovery from scratch and getting it wrong.

Jito bundles change the protection model. On Solana you don't bid for block position with gas; you submit a bundle with an explicit tip to a Jito-enabled validator, with the guarantee that nothing else gets inserted between your instructions in that bundle. For arbitrage, this is the difference between an atomic two-leg trade and a half-filled position you have to unwind manually. Vexor's Solana execution path uses bundle submission where appropriate so the buy-leg and sell-leg either both land or neither does — there is no "got the buy, missed the sell" failure mode.

Consolidated infrastructure removes most of the operational tail. Vexor runs Solana through a single multi-chain QuickNode RPC with WebSocket subscriptions for state changes, the same `vx-core` gateway that proxies the rest of the platform, and the same AI Risk Engine that gates the Snipe Method. That means an arb candidate has already been screened for honeypot patterns, serial-rugger deployers, and LP status before the engine is willing to route capital through it — which kills the most common loss scenario for cross-DEX arbs on long-tail tokens (arbing a real spread into a token that's actively being rugged from the other side).

Per-strategy slippage floors. The MEV mode's Conservative, Balanced, Aggressive, and Quantum strategies each have their own slippage floor enforced server-side. Aggressive and Quantum raise intensity multipliers and capital deployment, but they do not silently raise the slippage you're willing to accept past the configured floor for that mode. This is the single biggest difference between an MEV system and a generic arb script: you can dial up aggressiveness without losing the bound that prevents you from becoming the sandwich victim of someone else's bot.

A realistic 2026 arb playbook

- Stop hunting USDC/WETH spreads on Ethereum L1 by hand. They are fully searcher-saturated.

- For cross-chain and long-tail spreads, model gas + tip + slippage before the trade. If gross spread isn't ≥ 2× total costs, skip it.

- On Solana, route through Jupiter V6 — it aggregates Pump.Fun curves, Raydium, Orca, and Meteora, which is where most viable spreads now live.

- For passive extraction, use a system like the Vexor MEV mode where strategy selection, slippage floors, and extraction telemetry are exposed and enforced server-side.

- Verify every candidate token through the Vexor Token Scanner before pointing capital at it — arbing into a honeypot or a freshly-rugged pool is the most expensive way to learn this lesson.

For strategy mechanics, capital minimums per mode, and the slippage floor logic, see the Vexor FAQ.

DeFi arbitrage in 2026 is a numbers game with thin margins and hostile competition. The edge is no longer in spotting the spread — it's in honest cost accounting and routing through infrastructure that doesn't quietly hand your spread to the validator.